7 / 236

7 / 236

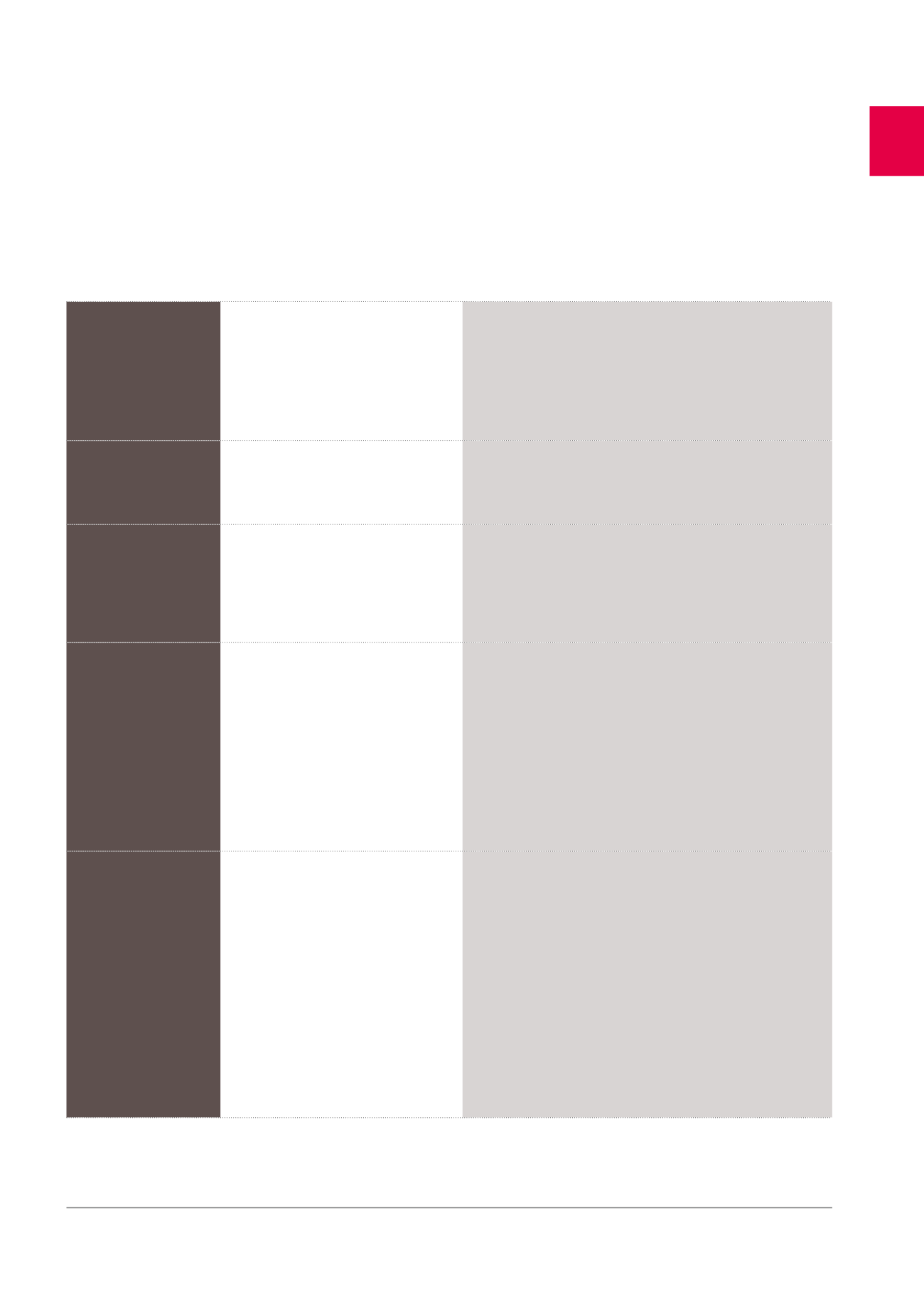

DESCRIPTION OF THE RISK POTENTIAL IMPACT

MITIGATING FACTORS AND MEASURES

Inappropriate choice

of investments or

developments

1. Change in the Group’s income potential.

2. Mismatch with market demand, resulting in

vacancies.

3. Expected yields not achieved.

Strategic and risk analysis and technical, administrative, legal, accounting

and taxation due diligence carried out before each acquisition. (1, 2, 3)

In-house and external valuations (independent experts) carried out for

each property to be bought or sold. (1, 2, 3)

Marketing of development projects before acquisition. (1, 2, 3)

Excessive own account

development pipeline

Uncertainty regarding future income.

Activity limited to maximum 10% of the fair value of the portfolio.

Poor management of major

works

1. Budget and timing not respected.

2. Increase in costs and/or reduction in

income; negative impact on the profitability

of the projects.

Specialised in-house Project Management team. (1, 2)

Specialised external project managers selected for the larger projects.

(1, 2)

Negative change in the fair

value of the properties

Negative impact on the net result, the net

asset value and the debt ratio.

At 31.12.2015 a 1% value change would have

had an impact of around 31.34 million EUR

on the net result and around 1.57 EUR on the

intrinsic value per share (compared with

31.99 EUR million and 1.78 EUR at 31.12.2014).

It would also have had an impact on the debt

ratio of around 0.35% (compared with 0.44%

at 31.12.2014).

Property portfolio valued by independent experts on a quarterly basis

conducive to corrective measures being taken.

Clearly defined and prudent debt policy.

Investment strategy focusing on quality assets and offering stable

income.

Multi-asset portfolio subject to different valuation trends able to offset

one another.

Main asset representing only 2.7% of the portfolio (see page 34).

Negative change in the fair

value of property assets

on the company’s ability to

distribute a dividend

Total or partial incapacity to pay a dividend if

the cumulative changes in fair value exceed

the distributable reserves.

The company has substantial distributable reserves, amounting to

168.4 million EUR.

These reserves allowed the Company to distribute a dividend for the

financial year 2014, even though the net income Group share was

negative.

In the past, the Group carried out certain transactions to allow it to

distribute its dividend: distribution of dividends by the subsidiary to

the parent company and restatement of non-distributable reserves,

corresponding to capital gains realised through mergers with the parent

company, as distributable reserves

1

.

PROPERTY PORTFOLIO

The Group’s investment strategy is reflected in a diversified portfolio of

assets with limited development activity for own account (construc-

tion of new buildings or complete renovation of existing buildings).

Occasionally, the company converts office properties at the end of

their operating period into apartments that it then puts up for sale.

The management of operating properties is carried out in-house by a

proactive team.

The asset diversification aims at a distribution of market risks.

1

As a reminder, the transfer of 214,087,000 EUR approved by the Extraordinary General Shareholders’ Meeting of 29.03.2011 has, on the one hand, increased the distributable amount by

an equivalent amount and made the total amount of the company reserves and the result carried forward of Cofinimmo SA/NV positive, and, on the other hand, reduced the combined

share capital and share premium account.

3