190 / 236

190 / 236

In accordance with its hedging policy, the Group hedges at least

80% of its portfolio of total debts for at least three years by entering

into interest rate derivatives (fixed listed IRS). The hedging period

of minimum three years was chosen, on the one hand, to offset the

depressive effect this time lag would have on the net income and,

on the other hand, to forestall the adverse impact of any rise in

European short-term interest rates not accompanied by a simulta-

neous increase in national inflation. Finally, a rise in real interest rates

would probably be accompanied or rapidly followed by a revival of the

overall economic activity which would give rise to more robust rental

conditions and subsequently benefit the net result.

The banks that sign these contracts are generally different from

the ones providing the funds, but the Group makes sure that the

periods of the interest rate derivatives and the dates at which they

are contracted correspond to the renewal periods of its borrowing

contracts and the dates at which their rates are set.

If a derivative instrument hedges an underlying debt contracted at a

floating rate, the hedge relationship is qualified as a cash flow hedge.

If a derivative instrument hedges an underlying debt contracted at a

fixed rate, it is qualified as a fair value hedge.

Below are the results of a sensitivity study of the impact of changes

in rate; the impact comes mainly from the change in the fair value

of derivative financial instruments and the change in floating-rate

credits.

Credit risk

By virtue of Cofinimmo’s operational business, it deals with two

main counterparties: banks and customers. The Group maintains a

minimum rating standard for its financial counterparties. All financial

counterparties have an external investment grade rating. Customer

risk is mitigated by a diversification of customers and an analysis of

their solvency before and during the lease contract. Also see pages

36 and 63 of this Annual Financial Report, which contains a table with

the top ten customers and their rating as assigned by an external

rating agency.

Price risk

The Group could be exposed to a price risk linked to the Cofinimmo

stock options tied to its convertible bonds. However, given that this

option is out-of-the-money, the risk is considered unlikely.

Currency risk

The Group is not currently exposed to any currency risk.

Liquidity risk

The liquidity risk is limited by the diversification of the financing

sources and by the refinancing which is done one year before the

maturity date of the financial debt.

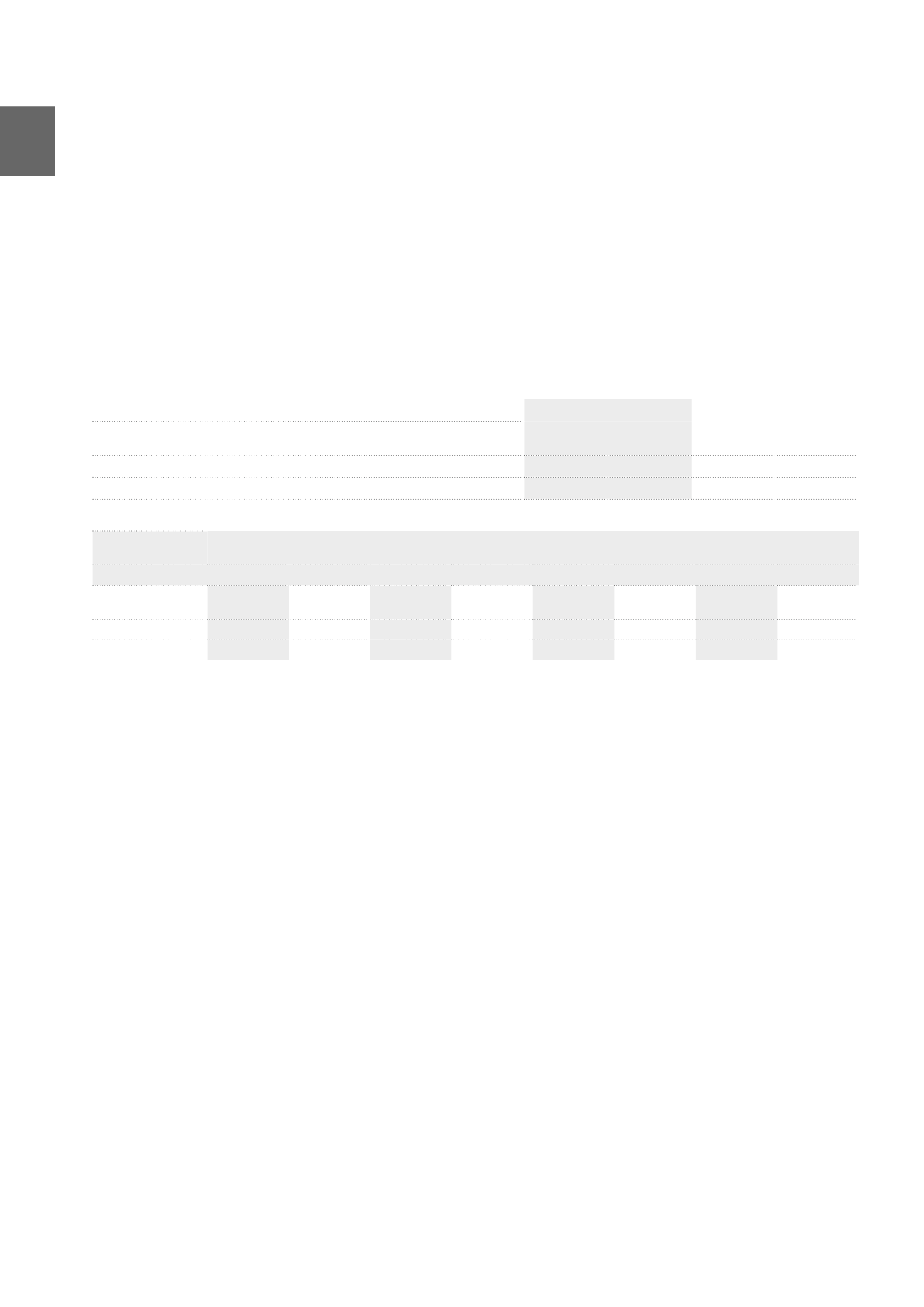

Summary of the potential effects, on equity and on the income statement, of a 1% change in the interest rate resulting from changes in

the fair value of the financial instruments (derivatives + convertibles), changes in the floating payments of the financial derivatives and

changes in the floating-rate credits.

(x 1,000 EUR)

2015

2014

Variation

Income

statement

Equity

Income

statement

Equity

+1%

41,141

0

57,442

7,171

-1%

-45,966

0

-37,791

-13,135

(x 1,000,000 EUR)

Change

Changes in the fair value of

the financial derivatives

Changes in the fair value of

the convertible bonds

Changes in floating payments

of the financial derivatives

Changes in floating-rate

credits

2015

2014

2015

2014

2015

2014

2015

2014

Fair value

at 31.12

-85

-125

388

381

-7

-18

-7

-13

+1%

51

67

5

9

-2

-9

-13

-25

-1%

-27

-44

-5

-9

-13

-20

-1

-11

186

ANNUAL ACCOUNTS /

Notes to the consolidated accounts